In a Nutshell:

Factory data still favour Asia over Europe, while PMIs say activity is expanding but rarely carefree. Inventory-protection buying, cost pressure and longer lead times are lifting demand, yet they are also making investment committees fussy. For machine vision, that means better order flow than the headlines imply – and a sharper focus on fast payback, yield, and resilience.

Followers of our social media profiles and members of our VisionCrunch community, are already familiar with the economic indicators we use to monitor the manufacturing industry by country. If you are not, please check out this explanation of Manufacturing PMI and year-over-year change in Industrial Output.

Purchasing Managers’ Index™ and PMI® are either trademarks or registered trademarks of S&P Global Inc or licensed to S&P Global Inc and/or its affiliates.

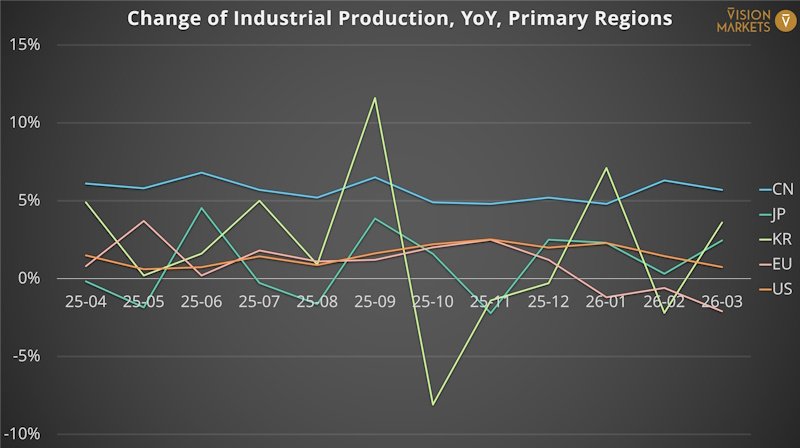

Regional Trends in Industrial Output

Industrial output remains a regional beauty contest with no unanimous winner. Over the latest three available prints, China cooled from 6.3% to 4.1%, still the strongest of the primary regions. The US stayed positive at 1.4%, Japan held a firmer 2.1%, and Korea recovered from a February dip to 1.5%. Europe, by contrast, slipped back to -2.1% dragged down by Germany’s -3.0%. Translation for automation budgets: Asia still looks like the better home for capacity additions; Europe still looks more like a retrofitting gym than a greenfield party.

Find always the latest charts on economic indicators in this blog post.

Sentiments in the Global Manufacturing Sector

Global: expansion with a precaution label – The global PMI held at 52.6 in May, its tenth month above the neutral line, while manufacturing production rose at the quickest pace since July 2021. That sounds like a cheerful marching band until one reads the footnotes: The analyses tell part of the lift came from clients front-loading orders to avoid higher prices and supply disruption, and input costs rose at the fastest pace since June 2022. In plain English, factories are busy, but some of that busyness smells suspiciously like stocking the cellar before the storm. For automation and machine vision that is still commercially useful. Insurance buying is still buying, especially where projects improve throughput, yield and labour efficiency. What it does not yet guarantee is a carefree wave of discretionary greenfield capex.

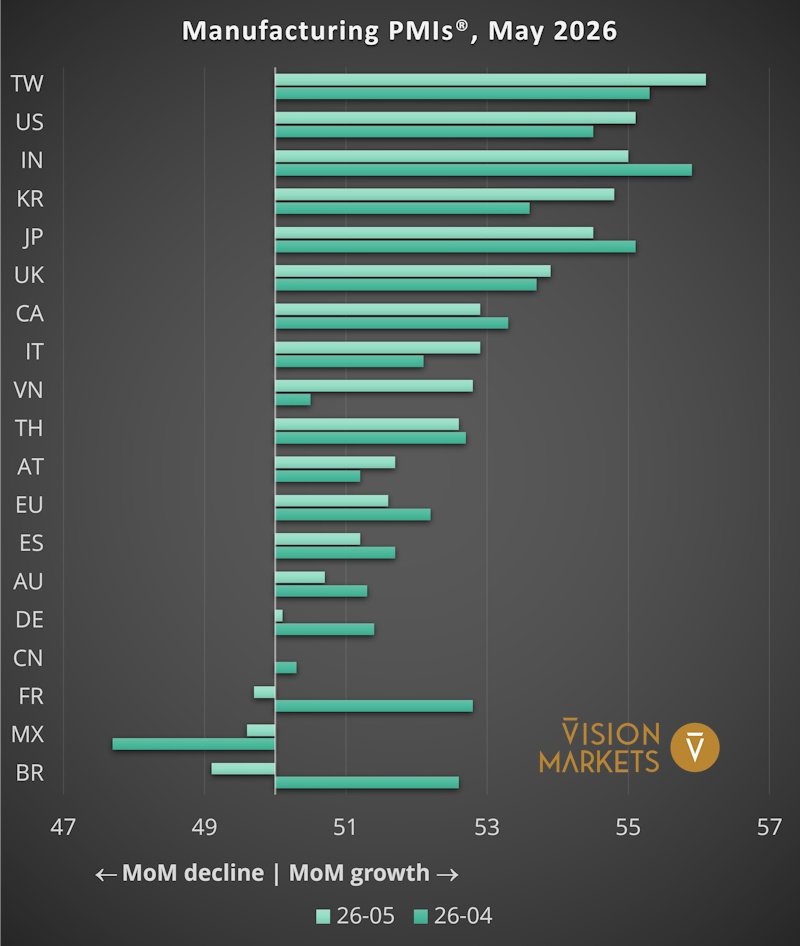

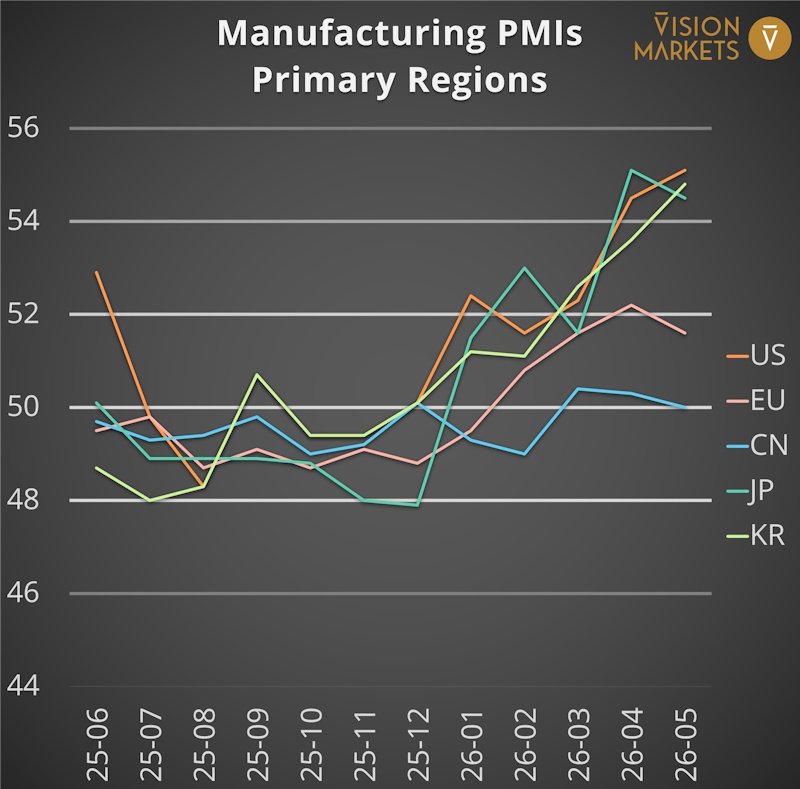

United States: a factory revival, with inventory fingerprints – The US PMI climbed to 55.1 in May from 54.5 in April, the highest reading since May 2022. Output posted its strongest upturn since April 2022 and firms added to finished-goods stocks for a second straight month. That would be unambiguously bullish were it not for the equally loud side-notes: input costs rose at the fastest pace since July 2022, delivery times deteriorated to the greatest extent since August 2022 and exports fell for an eleventh consecutive month as tariffs and geopolitics hurt foreign sales. The result is good news with a small asterisk wearing steel-toe boots. For machine vision suppliers, the US still looks constructive because brownfield productivity upgrades, traceability, scanning and in-line inspection remain easier to approve than cathedral-sized new factories. If the inventory wave fades before exports recover, growth may cool; for now, demand is real enough to keep order books warm.

Eurozone: expansion, but not the carefree kind – Eurozone manufacturing stayed in expansion at 51.6 in May, yet the mood lost momentum after April’s stronger run. New orders stagnated, export demand softened and production growth slowed to its weakest pace since January. At the same time, input costs rose at the steepest rate since May 2022 and output price inflation hit a three-and-a-half-year high. The awkward wrinkle is that worsening delivery times still contributed positively to the headline PMI, because the index treats longer lead times as historically associated with stronger demand. This is why Europe currently resembles a runner on a moving walkway: advancing, yes, but with a machine tugging at the shoelaces. For machine vision players, Europe remains a market for upgrade logic rather than exuberance. Projects that defend margins, save labour or stabilise quality can pass the committee test; broad, confidence-led spending still looks less reliable than the PMI headline might suggest.

China: steady expansion, broader exuberance not invited – China’s PMI eased to 51.8 in May from 52.2, still above 50 for a sixth consecutive month. New orders and output remained robust and among the stronger readings of recent years, while inflation pressure softened for the first time in six months. That is the pleasant half of the story. The less romantic half is that export business slipped, employment contracted marginally and delivery times lengthened for a third month, prompting another rise in input stocks. China still looks investable for automation, but increasingly in the disciplined, selective sense: quality improvement, yield, productivity and bottleneck removal remain attractive; generic “China is back, send brochures” strategies do not.

Japan: genuine strength, with safety stocks in the luggage – Japan’s PMI slipped from April’s 55.1 to 54.5 in May, which is rather like complaining that champagne has become only very good. Output and new orders still rose strongly, export orders improved at the fastest pace in five years and hiring stayed solid. Yet the survey is explicit that part of the expansion reflects stock building by manufacturers and customers safeguarding against shortages and price risk. Costs and selling prices rose at some of the steepest rates seen in more than two decades of data. That mix matters for machine vision. When output, orders and hiring all improve together, demand broadens beyond basic automation toward quality control, metrology and semiconductor-related applications. Japan still looks like one of the more convincing bright spots this month, even if the sprint is being run with a backpack full of contingency stock.

South Korea: semiconductor muscle, cost-side headaches – South Korea’s PMI rose to 54.8 in May from 53.6, the highest since March 2021. Output and new orders posted their strongest growth in around five years, while employment rose at the fastest pace since March 2013. Again, the report asks readers not to confuse momentum with serenity: stock building linked to price and supply disruption remains a major driver, input cost inflation stayed close to record highs and lead times remained deeply stretched. In practical terms, this is still fertile ground for machine vision because Korea’s electronics and semiconductor exposure gives automation spending unusually hard economic logic. When fabs and electronics lines chase capacity, yield and speed, vision tends to be invited early to the meeting. The risk is not a sudden collapse in interest; it is margins becoming tight enough to prune the decorative projects while protecting the crucial ones.

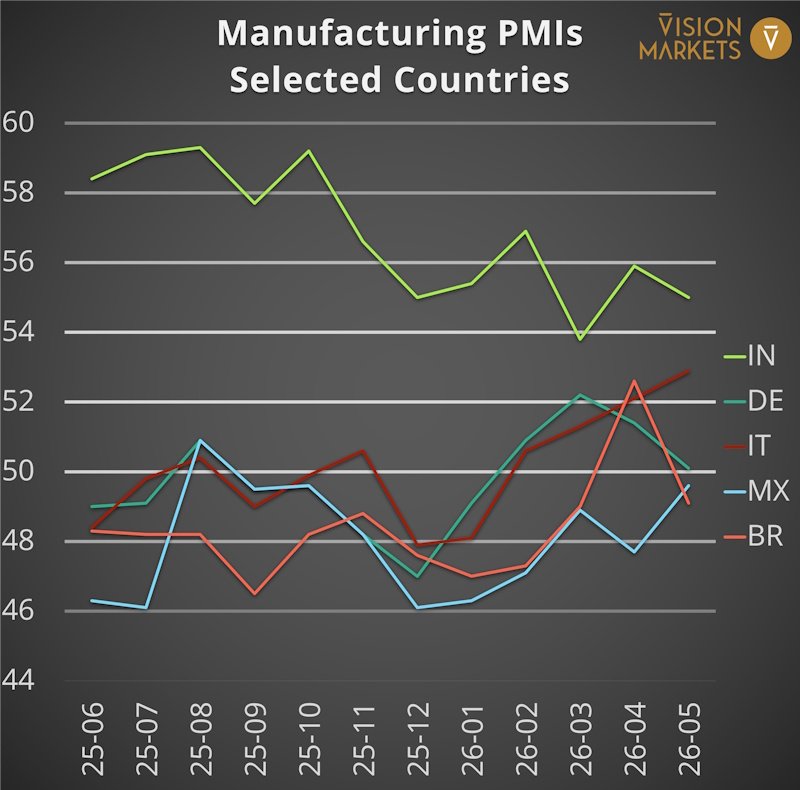

India and ASEAN: India still builds, ASEAN cools – India and ASEAN continue to tell related but no longer identical stories. India’s PMI rose to 55.0 in May, with faster output and order growth, support from domestic demand and infrastructure projects, and further stock building despite sharply elevated input costs. Competitive pressure, however, limited the pass-through into prices, hinting at some margin squeeze. ASEAN, by contrast, slowed to 50.7 in April, the weakest reading in nine months. Output growth nearly stalled, export orders fell at the fastest pace since last July, inventories were drawn down and employment slipped. For machine vision suppliers, that implies a useful divergence inside Asia ex-China: India still looks like a capacity-build and localisation story, while ASEAN remains strategically important but presently tilts toward faster-payback, modular investments rather than “build first, justify later” capital adventures.

What we’ll watch next month:

Whether inventory-led strength turns into genuine end-demand; whether Europe’s cost squeeze eases; and, with Q2 approaching, whether the next set of company reports confirms that semiconductors and electronics remain the most caffeinated customers in the room.

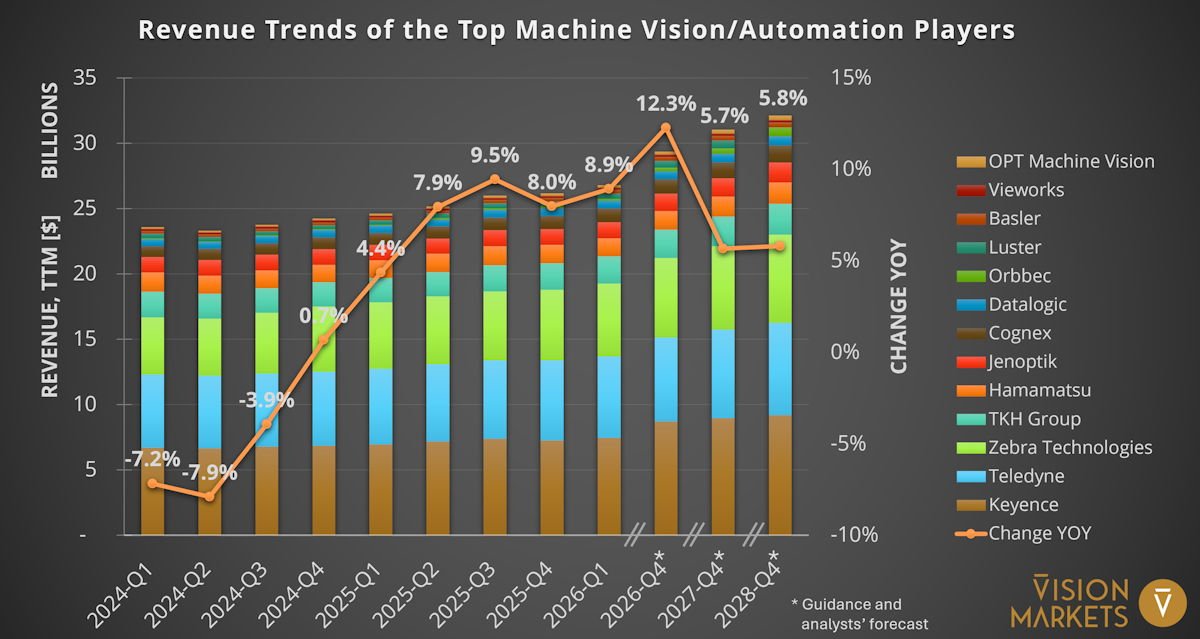

Revenue Trends of Key Players

Disclaimer: For information purposes only. No investment advice!

The revenue scoreboard still says growth, but the leadership remains concentrated. Our basket of listed suppliers with a meaningful machine vision business points to 12.3% annual TTM growth in 2026 and 5.7% in 2027. For full-year 2026, the three fastest growers are Orbbec (+100.0%), Luster (+30.2%) and OPT Machine Vision (+26.3%). At the other end sit Vieworks (+2.7%), Datalogic (+4.4%) and Hamamatsu (+4.9%). The pattern is hard to miss: Chinese-headquartered challengers dominate the top of the table, while more mature diversified players cluster in low single digits. For the latest fully available quarter, 2026-Q1, the leaders are Orbbec (+49.5%), OPT Machine Vision (+48.5%) and Basler (+31.7%); the laggards are Hamamatsu (+2.3%), Jenoptik (+3.0%) and Vieworks (+6.4%). The latest file raised 2026-Q4 expectations sharply for Orbbec (+24.8 percentage points), with smaller upward nudges for Luster and OPT Machine Vision, while Vieworks, Basler and Hamamatsu saw the largest downticks. Commercially, the message is not “everyone wins”; it is “the capable specialists in electronics-heavy and China-anchored segments are winning more”.

Implications for Machine Vision players:

Setting a strict focus in sales and marketing is the biggest lever – Machine vision demand is improving, but not democratically. Regions and applications with the clearest productivity logic are attracting budgets first, while cost pressure, delivery risk and geopolitics keep broader capex on a short leash. If you want to benchmark your product focus, pipeline or regional exposure against these shifts, let’s talk before the next budget round turns into theatre.