In a Nutshell:

Industrial output still favors Asia over Europe, while the latest June PMIs show expansion continuing globally, lacking that swagger, still. Inventory protection, export uncertainty and cost pressure are shaping capex decisions. For machine vision, that means demand remains real – just far more selective and brutally ROI-focused.

Followers of our social media profiles and members of our VisionCrunch community, are already familiar with the economic indicators we use to monitor the manufacturing industry by country. If you are not, please check out this explanation of Manufacturing PMI and year-over-year change in Industrial Output.

Purchasing Managers’ Index™ and PMI® are either trademarks or registered trademarks of S&P Global Inc or licensed to S&P Global Inc and/or its affiliates.

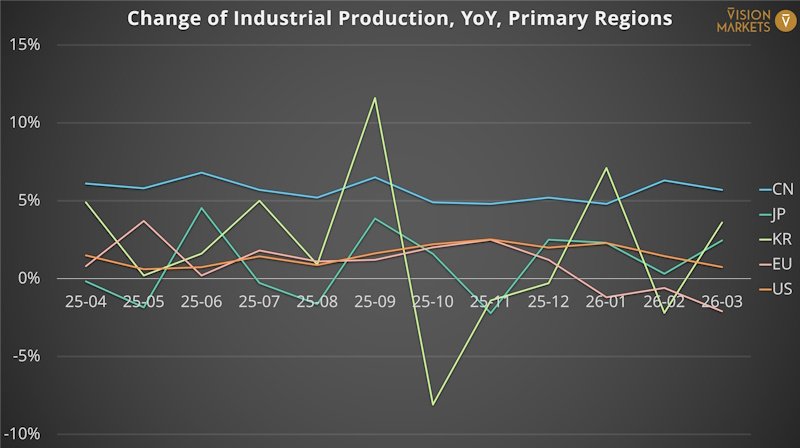

Regional Trends in Industrial Output

Industrial output remains a regional beauty contest with no unanimous winner. Over the latest three available prints, China cooled from 6.3% to 4.1%, still the strongest of the primary regions. The US stayed positive at 1.4%, Japan held a firmer 2.1%, and Korea recovered from a February dip to 1.5%. Europe, by contrast, slipped back to -2.1% dragged down by Germany’s -3.0%. Translation for automation budgets: Asia still looks like the better home for capacity additions; Europe still looks more like a retrofitting gym than a greenfield party.

You can always find the latest charts on economic indicators in this blog post.

Sentiments in the Global Manufacturing Sector

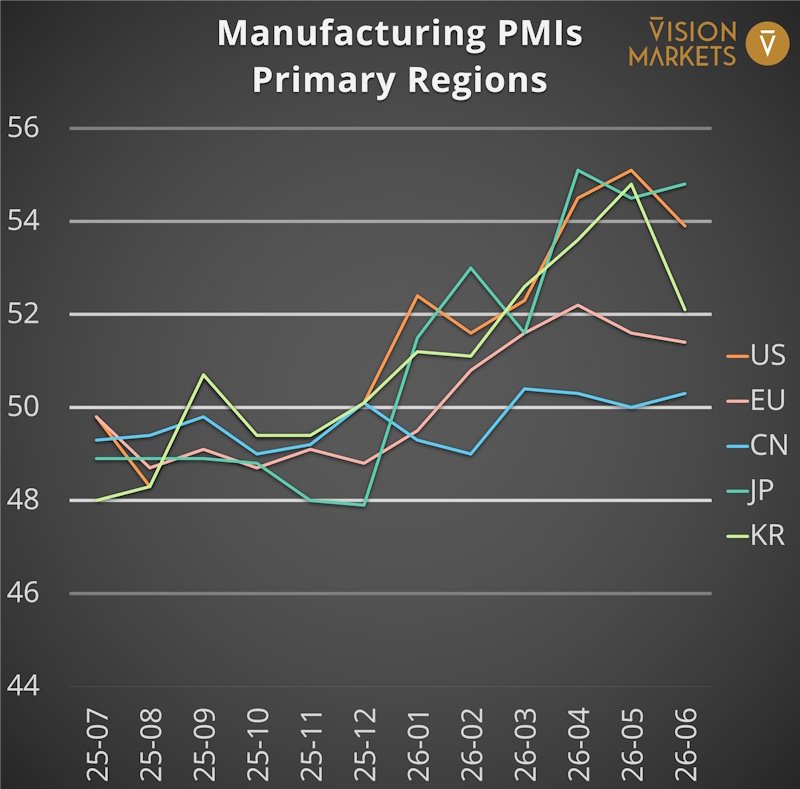

Global: expansion with a precaution label – The global PMI held at 52.6 in May, its tenth month above the neutral line, while manufacturing production rose at the quickest pace since July 2021. That sounds like a cheerful marching band until one reads the footnotes: The analyses tell part of the lift came from clients front-loading orders to avoid higher prices and supply disruption, and input costs rose at the fastest pace since June 2022. In plain English, factories are busy, but some of that busyness smells suspiciously like stocking the cellar before the storm. For automation and machine vision that is still commercially useful. Insurance buying is still buying, especially where projects improve throughput, yield and labour efficiency. What it does not yet guarantee is a carefree wave of discretionary greenfield capex.

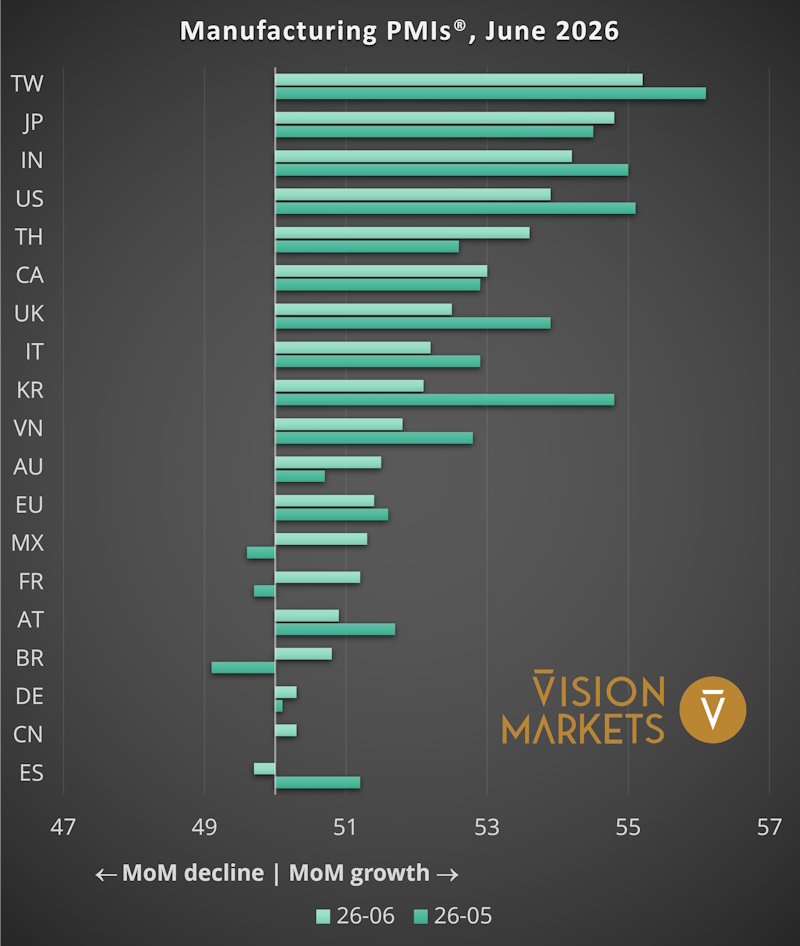

United States: Orders still rise, exports still sulk – The United States posted 53.9 in June, down from 55.1. Output and new orders remained strong, helped by product launches and pre-orders designed to outrun price increases, yet exports fell for a twelfth straight month. Employment was the weak flank, with the sharpest job shedding since May 2020, while confidence slipped to the lowest since October 2025. The machine vision implication is almost textbook American manufacturing in 2026: domestic factories are still spending where automation protects margins and labor productivity, but broad optimism keeps giving way to a more tactical style of purchasing. Brownfield upgrades still pass; cathedral-sized capex now needs a much more persuasive sermon.

Eurozone: Output improves, confidence still needs caffeine – The eurozone PMI edged down to 51.4 in June from 51.6, a four-month low, though output growth actually improved to a two-month high. New orders turned marginally positive, but export demand declined for a second month. Supply conditions remained stretched and manufacturers continued to run down inventories. Encouragingly, cost and output-price inflation both eased. Particularly useful here: the region has benefited from precautionary stockpiling, and if that fades, it could become a drag in the coming months. In machine-vision terms, Europe is not collapsing; it is bargaining. Projects that save labor, protect yields or stabilize production quality remain investable. Expansion for expansion’s sake still feels like a luxury item.

China: Still expanding, just with a raised eyebrow – China’s PMI slipped fractionally to 51.7 from 51.8, but June completed the strongest quarter since late 2020. New orders rose for the thirteenth consecutive month, employment increased at the fastest pace since August 2023, and cost inflation eased to a five-month low. The weak patch remains external demand: export business fell again and business sentiment softened to the lowest since January. That combination matters. China is still investable for automation where suppliers can improve yield, output and labor efficiency, especially in electronics-related operations. But the old fantasy that ‘China strength lifts everyone equally’ belongs in the museum next to surplus optimism and free coffee at trade fairs.

Japan: A genuinely strong quarter, with inventory fingerprints all over it – Japan improved to 54.8 in June from 54.5, rounding off its strongest quarter since Q1 2014. New orders rose at the fastest pace since early 2022, helped by AI-related technology and semiconductor demand. Yet the survey is refreshingly blunt: clients are also building inventories because the Middle East conflict continues to disrupt supply chains and keep prices elevated. This is exactly the kind of environment in which machine vision often gets pulled forward – inspection, metrology and high-value process control are easier to justify when factories are running hard and shortages make mistakes expensive. The caveat is obvious: if the stockpiling sugar rush fades, some of the short-term excitement will fade with it.

South Korea: Still positive, but no longer sprinting – South Korea fell back to 52.1 from 54.8. That still signals growth, but the move is a reminder that the second quarter’s fireworks have become a steadier glow. New orders rose at the slowest pace of the year and exports weakened again, while production growth also softened. Price and supply pressures remained pronounced, employment fell, and confidence slipped to a seven-month low. The good news for machine vision is that Korea’s semiconductor and electronics base still gives automation spending strong economic logic. The bad news is that cost pressure and delivery delays tend to prune decorative projects first. Expect continued demand – but with less room for indulgence.

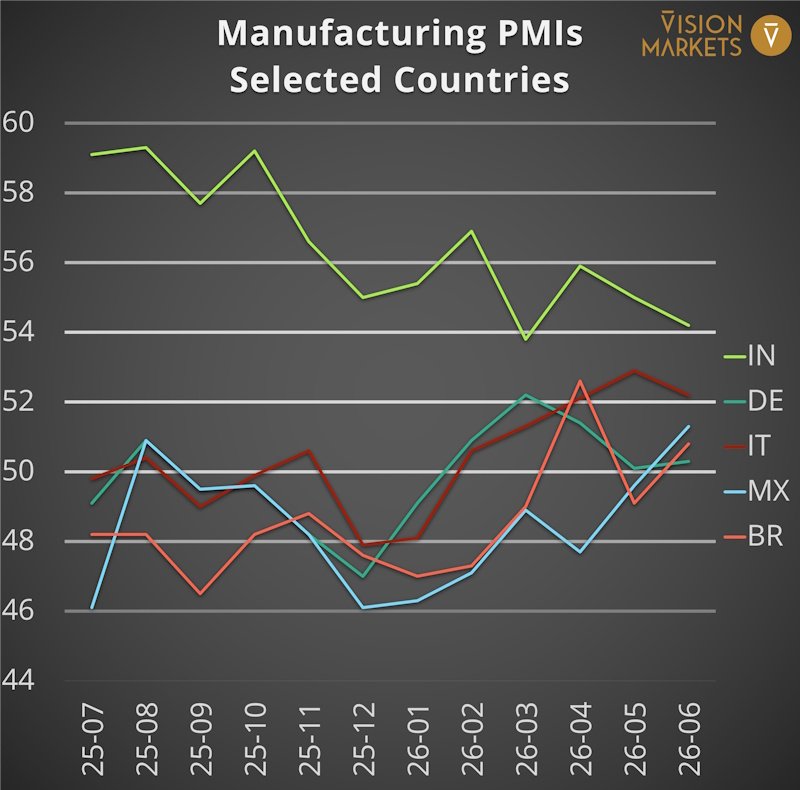

India and ASEAN: One still builds, the other catches its breath – India cooled to 54.2 from 55.0, still strong but with output, new orders, exports and hiring all slowing. Analyses note that the easing partly reflects the fading of the earlier boost linked to Middle East-related disruption. Capital goods were the main source of the moderation. ASEAN weakened more clearly, sliding to 50.5 from 51.5, its lowest level in eleven months. New orders and production softened, export orders fell sharply, and staffing fell again. For machine vision suppliers, the divergence is becoming useful: India still looks like a market for capacity build-out and localisation, while ASEAN increasingly favors modular, faster-payback investments over ambitious all-at-once expansion plans.

What we’ll watch next month:

Watch whether June’s slight average PMI cooling proves to be healthy normalisation and constitutes a broad global upswing or if this is the start of a general comedown. We will also monitor if Europe’s easing cost pressure is enough to revive confidence-led capex, and - now that the next month opens a new reporting rhythm - whether Q2 company results confirm that semiconductors remain the market’s loudest customer.

Implications for Machine Vision players:

Machine Vision demand is improving, but it is improving with conditions attached. The winners are increasingly those aligned with fast-payback automation, electronics-heavy demand, and regions where factories are still willing to spend before they feel entirely comfortable. If you want to benchmark your product focus, regional exposure or growth options against these shifts, let’s talk before the next budget round turns market uncertainty into corporate theatre.