The global manufacturing sector displayed varied trends in June. The US showed strong recovery with a Manufacturing-PMI of 52.9, driven by new orders and domestic demand. The Eurozone continued to contract at 47.5, with easing inflationary pressures. Germany reached a 34-month high at 49.0, yet still in contraction. Japan stabilized at 50.1, with modest production increases. China returned to growth at 50.4, despite weak export orders. South Korea faced subdued conditions at 48.7, but optimism for the year ahead rebounded strongly. India demonstrated continued growth at 58.4, fuelled by strong demand and export orders.

This report delves into the latest Manufacturing PMI figures for the major target markets of manufacturing automation and machine vision including the US, EU, China, Japan, South Korea, and India, highlighting significant changes in order income, stock levels, and other critical developments that shaped the sentiment of the manufacturing sector.

Followers of our social media profiles and members of our VisionCrunch community, are already familiar with the economic indicators we use to monitor the manufacturing industry by country. If you are not, please check out this explanation of Manufacturing PMI and year-over-year change in Industrial Output.

Purchasing Managers’ Index™ and PMI® are either trademarks or registered trademarks of S&P Global Inc or licensed to S&P Global Inc and/or its affiliates.

On the global level, manufacturing picked up in June, with the Output index rising to 51.3, the strongest since February. The New Orders index also edged into expansion territory at 50.1, led by improvements in China and the US. However, Export Orders remained in slight contraction at 49.3. Employment continued to decline but at a slower pace.

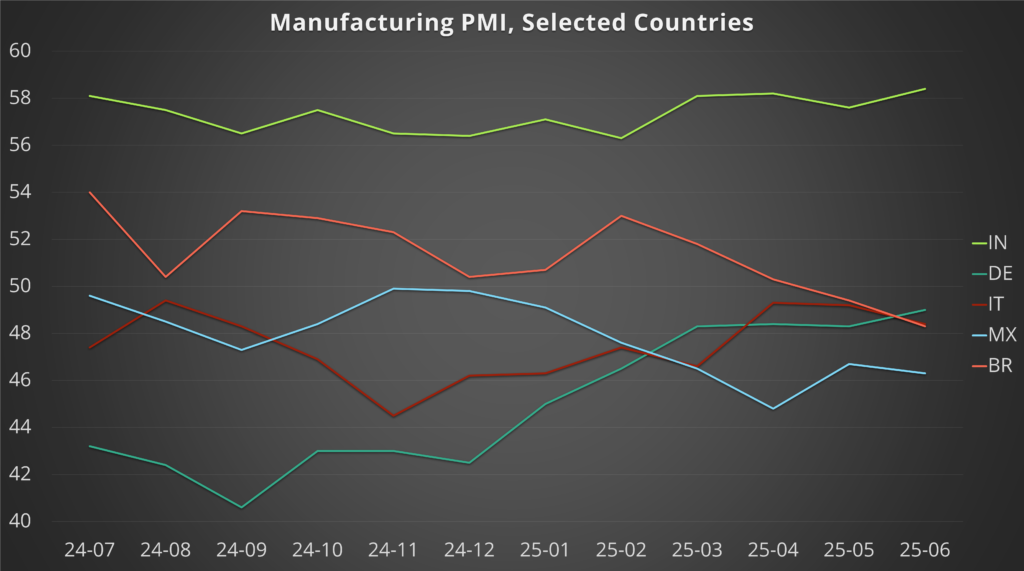

Figure 1 shows the latest readings of the most relevant target economies for industrial automation and machine vision.

Fig. 1: Latest Manufacturing PMI readings of target countries of Machine Vision and Industrial Automation from June 2025

United States: Continued Positivity while Tariffs Drive Input Costs

The US Manufacturing PMI climbed to 52.9, the highest among G7 peers, signalling a continuing recovery from a long period of declines. Growth was fuelled by surging new orders, improved domestic demand, and robust production. The labour market strengthened further, with manufacturers ramping up hiring to support increased activity. Input and output prices rose sharply, reflecting inflationary pressures from tariffs, wages, transportation, and raw materials.

Key trends in U.S.’s manufacturing sector:

- New Orders: New orders rose for the sixth consecutive month, driven by both domestic and international demand. Export orders also increased modestly, though growth was partially constrained by tariffs.

- Output: Manufacturing output rebounded in June after three months of decline, marking the strongest growth since early 2024. This was largely attributed to higher order volumes and successful marketing efforts.

- Inventories: Firms increased input purchases significantly – the most in over three years – partly to build inventories in anticipation of tariff-related price hikes. This led to a continued rise in pre-production stock levels.

- Prices: Input costs surged due to tariffs, pushing inflation to its highest in nearly three years. Manufacturers passed these costs on to customers, raising output prices sharply.

- Labour: Employment grew at the fastest pace since late 2022, supported by improved business confidence and rising backlogs.

Eurozone: Continued Contraction with Easing Inflationary Pressures

The Eurozone manufacturing sector continued to contract in June, with the Eurozone Manufacturing PMI registering 47.5, in insignificant improvement from May’s 47.3 but still firmly below the 50.0 mark. This indicates a persistent downturn, albeit at a slightly softer pace. The contraction was broad-based across the region, with Germany and France remaining significant drags.

New orders continued to fall, reflecting weak demand conditions both domestically and internationally. This led to further reductions in production and employment. However, a positive development was the continued easing of inflationary pressures, with both input costs and output charges declining, offering some relief to manufacturers.

As Europe’s manufacturing sector with the highest sentiment score, Spain saw improved operating conditions in June. Production rose solidly, new orders increased for the first time since January, hiring remained steady, and business confidence reached its highest level since February.

Key trends in Eurozone’s manufacturing sector:

- New Orders and Output: Continued decline in new orders led to further reductions in output. The rate of contraction in new orders was significant, impacting production volumes across the region.

- Employment: Firms continued to shed jobs, though the pace of job losses eased slightly. This reflects ongoing efforts to align workforce levels with reduced demand and the continued automation of shop floors.

- Inventories: Stocks of finished goods continued to rise as sales remained subdued, while stocks of purchases were reduced in line with lower production requirements.

- Prices: Input cost inflation eased further, and output charges also declined, indicating a disinflationary trend.

Japan: Stabilisation Amidst Subdued Demand

Japan’s manufacturing sector showed signs of stabilization in June, with the S&P Global Japan Manufacturing PMI rising to 50.1 from 49.4 in May. This marks the first time the index has been above the neutral 50.0 level in 11 months, indicating broadly stable operating conditions. While production saw a fresh rise, demand conditions remained subdued, with both new orders and export sales continuing to decline. Despite this, business confidence improved, and firms increased their payroll numbers, anticipating future activity.

Key trends in Japan’s manufacturing sector:

- Output: Production increased for the first time in ten months, albeit modestly, driven by hopes of improved customer demand and efforts to reduce backlogs.

- New Orders and Exports: Overall demand remained subdued, with a further decline in new orders and export sales. Lower demand from key markets in Asia, Europe, and the US was noted.

- Inventories: Companies remained cautious with inventory levels, with stocks of finished goods falling slightly and inventories of inputs rising only fractionally.

- Employment: Employment continued its upward trend, with the latest upturn being the most pronounced in 14 months, driven by filling vacancies and expectations of firmer customer demand.

- Prices: Input cost inflation accelerated slightly in June, remaining sharp overall, leading to a solid increase in selling prices as companies passed on higher cost burdens.

South Korea: Deterioration Slows, Optimism Rebounds

South Korea’s manufacturing sector continued to face subdued conditions in June, with the S&P Global South Korea Manufacturing PMI rising to 48.7 from 47.7 in May. While still indicating contraction, this marks the softest deterioration in three months. Both output and new order intakes continued to decline, albeit at a slower rate. A notable development was the rebound in business optimism, reaching its strongest level in over a year, driven by hopes of an improved domestic economy and geopolitical landscape.

Key trends in South Korea’s manufacturing sector:

- Output and New Orders: Production volumes fell for the fourth consecutive month, and new order intakes declined for the third month in a row, including new export sales. However, the pace of these contractions eased.

- Employment: Employment levels saw a renewed fall, reversing the uplift seen in May, as firms continued to shed jobs.

- Inventories: Purchasing activity fell, and holdings of pre-production goods were lowered, reflecting a reluctance to hold excess inventories. Stocks of finished goods saw a modest depletion.

- Prices: Input cost inflation eased to an eight-month low, contributing to only a modest increase in selling prices. This was partly due to an improved exchange rate, easing price pressures on internationally sourced inputs.

- Business Optimism: Despite the ongoing contraction, business confidence for the year ahead strengthened significantly, reaching a 13-month high.

China: Return to Growth Amidst Export Weakness

China’s manufacturing sector returned to growth in June, with the Caixin China General Manufacturing PMI rising to 50.4 from 48.3 in May. This marks a significant improvement, indicating an expansion in manufacturing conditions. The renewed growth was supported by higher new order inflows and a rise in production. However, the pace of new order expansion was marginal due to subdued exports, which declined for the third consecutive month.

Key trends in China’s manufacturing sector:

- Production and New Orders: Manufacturing production expanded, and new orders returned to growth after a brief contraction in May. This was driven by firmer demand conditions and promotional activities.

- Export Weakness: Despite overall growth, new export orders continued to decline, reflecting persistent weakness in external demand, particularly from the US due to tariffs.

- Employment: Employment in the Chinese manufacturing sector fell, as companies prioritized cost control and efficiency. This led to a slight accumulation of backlogged orders.

- Prices: Input costs continued to decline for the fourth consecutive month, leading to a more pronounced fall in average selling prices. This was attributed to lower raw material prices and fierce market competition.

- Inventories: Stocks of finished goods were depleted slightly due to order fulfillment, while input stocks remained stable.

India: Surging Growth and Export Momentum

India’s manufacturing sector demonstrated robust performance in June, with the HSBC India Manufacturing PMI reaching a 14-month high of 58.4, up from 57.6 in May. This significant increase indicates a substantial improvement in the health of the sector, driven by strong demand and a surge in new export orders. Production volumes increased at the fastest pace since April 2024, and employment rose at a survey-record pace.

Key trends in India’s manufacturing sector:

- Output and New Orders: Production volumes increased rapidly, fueled by efficiency gains, favorable demand, and greater sales. New order inflows saw a quicker upturn, with a substantial rise in exports, particularly from the US.

- Employment: Employment rose at a survey-record pace, with companies pointing to short-term recruitment to keep up with robust sales.

- Inventories: Pre-production inventories rose, while inventories of finished goods fell as businesses had to dig into warehouses to fulfill demand growth.

- Prices: Input price inflation retreated to a four-month low, despite rising iron and steel costs. However, average selling prices rose markedly as firms passed on higher freight, labor, and metal costs to clients.

- Outlook: The outlook for the Indian manufacturing sector remained positive, though uncertainties surrounding competition, inflation, and consumer preferences were noted.

How to Navigate Times of Global Shifts and Uncertainty

June 2025 presented a complex and varied picture for the global manufacturing sector. The interplay of new orders, production volumes, employment trends, inventory management, and evolving price pressures continues to shape the landscape. As the global economy progresses, these PMI indicators will remain vital in understanding the ongoing shifts and informing strategic decisions within the manufacturing industry.

If you would like to learn more about

- our perspective on the global target markets of Industrial Automation and Machine Vision, or

- your success factors to survive and grow challenging market environments

please contact us.

Find the latest available readings of Manufacturing PMIs and the Industrial Output of the target countries of Machine Vision here.

Don’t miss our future market updates!

Subscribe to our VisionCrunch business newsletter today!