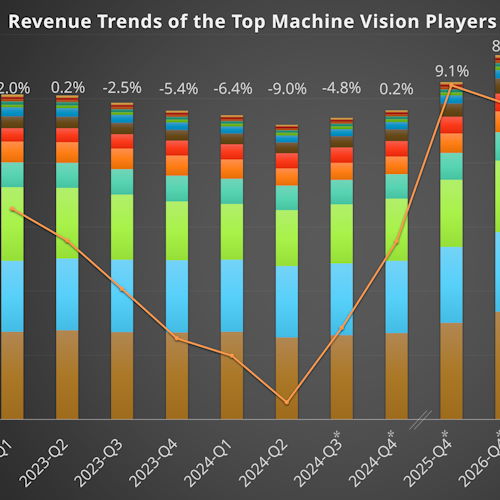

Our quarterly analysis of the revenue trends in Machine Vision sparks hope for a significant acceleration from sloppy revenues in the first half of 2024.

Disclaimer: The information presented in this chart is for informational purposes only and should not be construed as financial advice. The data is based on publicly available information and is subject to change. Past performance is not indicative of future results. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions. The creators of this chart are not responsible for any losses or damages arising from the use of this information.

Following a relatively stable trend in 2023, revenues experienced a significant decline in the first and especially the second quarter of 2024. Basler reported a year-over-year (YoY) decrease in its trailing twelve-month (TTM) revenue of 28.1% in Q2, while OPT Machine Vision saw a 27.8% drop. Similarly, Zebra Technologies, Stemmer Imaging, and Datalogic recorded declines ranging from 19.4% to 20.8% during the same period. In contrast, companies focusing more on vision solutions rather than components, such as Jenoptik, saw a growth of 9.4%, and Antares Vision reported a 3.5% increase.

Despite the significant slowdown in the first half of the year, revenue projections for 2024 remain relatively optimistic. Zebra Technologies is expected to achieve an annual revenue of $4.86 billion, up 6% from $4.58 billion in 2023. Cognex also forecasts an 8.5% revenue increase in 2024, despite reporting declines of 8.4% in Q1 and 5.5% in Q2. Similar trends are anticipated for the second half of 2024 across the board. For instance, Keyence is projected to have a YoY decline of just 0.5% by Q4 2024, compared to a 7.9% decline in Q2, and Basler is expected to see a decline of just 2.2%, indicating a significant recovery towards the end of the year.

For our Machine Vision Market Report, the revenues from machine vision components of the above players are just a few of over 120 insightful indicators we consider. Together with a network of 600 industry insiders, we provide detailed analyses of the machine vision market size and its trends by product type, region, industry, and combinations of such. To obtain the latest version of the report, please contact us.

How to Benefit from our Expertise

Do you want to be notified about all updates on the revenues of Machine Vision players, the top players from machine vision target markets such as industrial automation, semiconductor manufacturing, logistics, food and beverages, and other key business news for the Machine Vision market? We invite you to join the VisionCrunch community for the optimal development of your Machine Vision business!

Machine Vision is a key technology of the 21st century. It enables machines to perceive and understand objects or entire scenes following the same concept as human visual creatures. However, a breadth of core technologies are required for Machine Vision:

Semiconductor technology for image sensing

Optics for projecting a scene onto the image sensor

Photonics for illuminating the scene or measuring distances

Electronics for the read-out and pre-processing of the image sensor data

Communication engineering for transmitting video data at up to several 100 Gbit/s

Materials science for robust cabling that withstand millions of cycles of bending and torsion

High-performance computing to process and analyze the image or video data

Deep Learning as novel approach of image analysis

Only very few companies master more than one of these technologies. Hence, the Machine Vision supplier market is enormously scattered with thousands of SMEs. Just some of the players are stock listed and among the large stock-listed players, only a few are exclusively active in Machine Vision.

Still, the accumulated revenue of the trailing 12-month period and its year-over-year change of our selection of the top-13 players can provide you with a first approximation of the actual machine vision market trend (see Fig. 1, quarterly updated).

Disclaimer: The information presented in this chart is for informational purposes only and should not be construed as financial advice. The data is based on publicly available information and is subject to change. Past performance is not indicative of future results. Investors should conduct their own research and consult with a qualified financial advisor before making any investment decisions. The creators of this chart are not responsible for any losses or damages arising from the use of this information.

For our Machine Vision Market Report, the revenues from machine vision components of the above players are just a few of over 120 insightful indicators we consider. Together with a network of 600 industry insiders, we provide detailed analyses of the machine vision market size and its trends by product type, region, industry, and combinations of such. To obtain the latest version of the report, please contact us.

How to Benefit from our Expertise

Do you want to be notified about all updates on the revenues of Machine Vision players, the top players from machine vision target markets such as industrial automation, semiconductor manufacturing, logistics, food and beverages, and other key business news for the Machine Vision market? We invite you to join the VisionCrunch community for the optimal development of your Machine Vision business!

In a year marked by general elections in over 100 countries, including 8 of the 10 most populous nations, global political dynamics are in flux. The United States faces significant political turmoil ahead of a pivotal election. Concurrently, two active war zones and heightened tensions around Taiwan, the Philippines, and Korea add to the global instability. Central banks worldwide are navigating perfect storms, balancing financial systems in acute imbalance with the conflicting needs of the real economy.

2024 was anticipated to be challenging for leading economies, particularly the industrial sector and hence the Machine Vision industry. However, the recession in the manufacturing sectors of the EU and Japan has proven to be more prolonged and severe than expected. Additionally, the increase in production output, reported by Chinese official authorities, no longer benefits Western OEMs as it once did.

Disclaimer: The information provided in this article is for informational purposes only and should not be considered investment advice. The author is not a registered investment advisor and is not affiliated with any brokerage or investment firm. Investing in the stock market involves risk, including the loss of principal. Readers should conduct their own research and consult with a financial advisor before making any investment decisions.

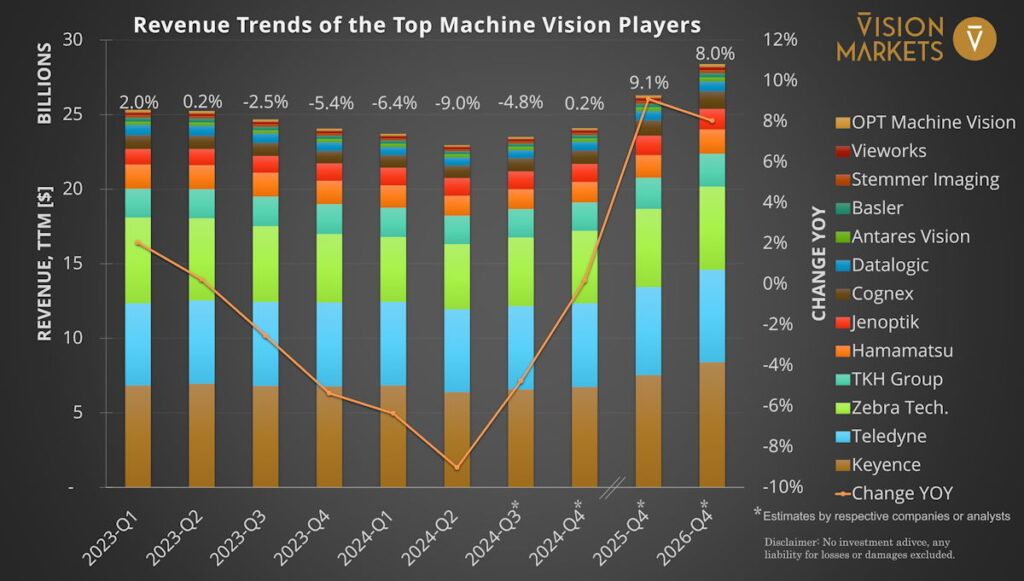

Fig. 1: Year-over-year change of industrial production output in the primary target regions of Machine Vision.

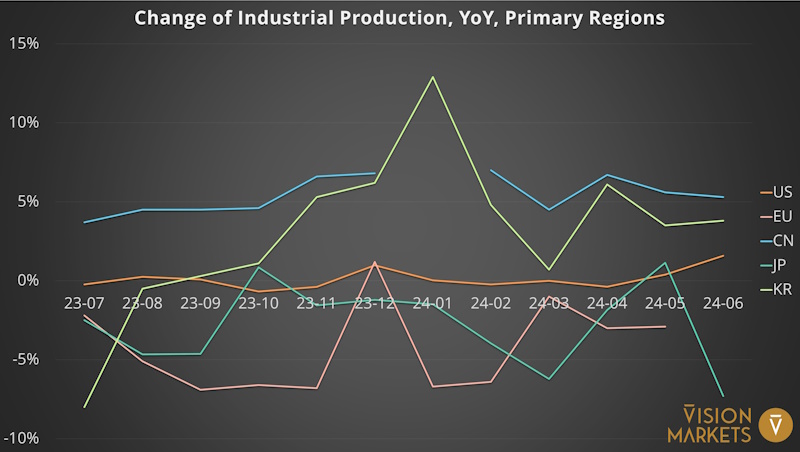

Fig. 2: Year-over-year change of industrial production output in the primary target regions of Machine Vision.

United States and Mexico

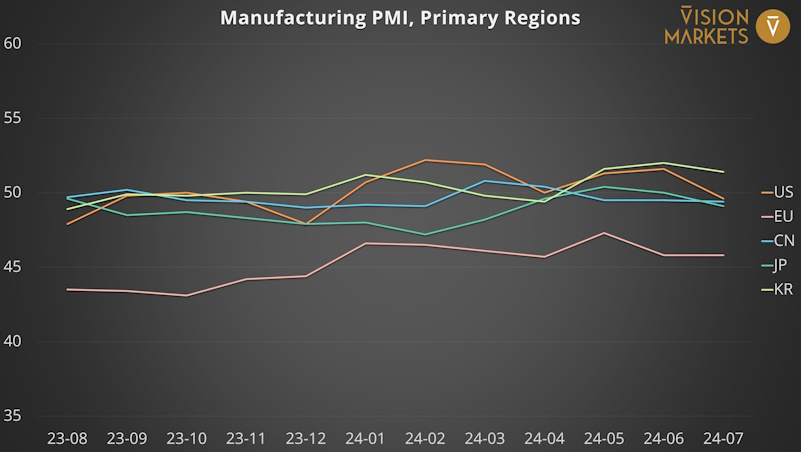

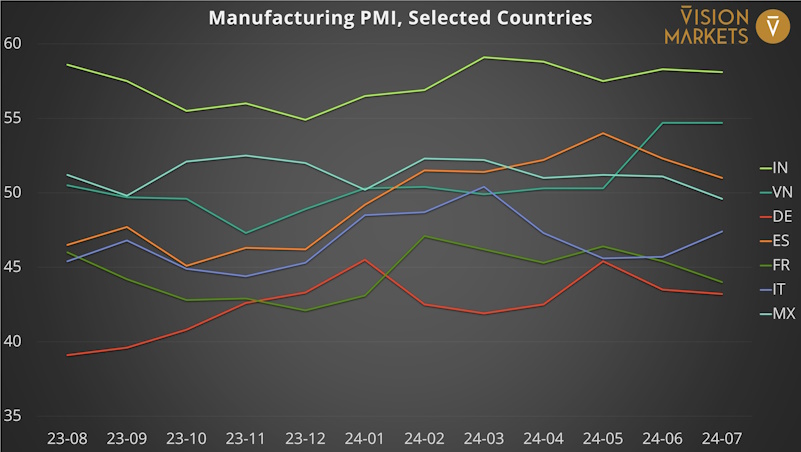

In June 2024, the US industrial production (light-orange line in Fig. 1 and Fig. 3) accelerated to the highest year-on-year growth rate since December 2022. The reading of 1.58% is still marginal but exceeds the H1’24 average of 0.23%, while June 2023 was also slightly above stagnation. Will this trend continue? Unfortunately, the July Manufacturing PMI for the US suggests otherwise, with a contraction reading of 49.6, coincidentally equal to Mexico (cyan line in Fig. 2 and Fig. 4). The Mexican Manufacturing PMI managed to stay in non-contracting territory throughout H1’24, although the year-on-year manufacturing output displayed high volatility, averaging 1.43% with a range from -3.0% to 5.1%.

The Biden administration released two major acts in 2022, totalling $400 billion in tax credits, loans, and grants, to bring manufacturing back to the US and decouple from China. However, a recent investigation revealed that approximately 40% of the projects funded by these acts have been delayed until after the November presidential election or paused indefinitely. The reasons are manifold:

Expected interest rate cuts by the Fed have been postponed to September/October 2024, making current investments unattractive.

Slower-than-expected demand for electric vehicles has led auto producers to delay expanding their production capacity.

China produces more EV batteries and about twice as many solar panels as global demand, causing eroding prices and unattractive investments in these sectors.

Some tax credit rules remain unclear, and Donald Trump has announced plans to cut down on such acts, leading to uncertainty and stalled investment activity, at least until November 2024.

The US government debt recently surpassed the $35 trillion mark. The unemployment rate rose for the fourth consecutive month to 4.3% in July. Despite new cycle highs in US manufacturing and construction employment, the pressure on the Fed to lower interest rates is immense to steer the economic development in a more positive direction. Should the conflict in and around Israel cool down, interest rates lower, policy certainty increase, and the semiconductor sector experience a cyclical upswing, the end of 2024 and all of 2025 could see positive developments for the North American manufacturing industry.

Fig. 3: Manufacturing PMI, primary target regions of machine vision.

Figure 4: Manufacturing PMI, selected target countries of machine vision.

Europe

The EU as a whole

(light-red line) has been in the recession zone of industrial production, with

rates mostly below -5% over the past 12 months. Germany, which hosts the

largest industrial sector among European economies, is leading this downward

trend with an M-PMI reading of just 43.1 in July and an average reading of 42.5

over the past year.

Following the recent general election in France, where the left-wing NFP won a slight majority, France is prone to instability with a policy gridlock despite the urgent need for political reforms. Concerns about the leftists’ impact on public debt and hence the Euro currency have caused the Euro and the CAC 40 stock market index to decline, while French government bond yields increased immediately after the election results. Additionally, the French M-PMI approached the detrimental levels seen in Germany in July, indicating a negative outlook for the Eurozone’s second-largest economy.

On a more positive

note, Spain and the UK are the only larger economies in Europe with

growth-indicating M-PMI readings for at least the three months from May to July

2024. Spain’s industrial production also showed a substantial year-on-year

increase, rebounding from a relatively weak 2023.

Japan and Korea

In March 2024, the Bank of Japan ended its policy of negative interest rates after eight years, while Japan’s public debt reached 238% of GDP amid an overaged population. The volatile Japanese Yen appreciated by around 10% against the USD in July alone, though this gain is insufficient to counteract its devaluation of up to 29% since March 2022. Such volatility not only has detrimental effects but also creates uncertainty, dampening investment activity. Japan’s industrial production (dark green line in Fig 1 and Fig. 3) plummeted by -7.3% in June, with an average decline of -3.28% in the first half of the year. The Manufacturing PMI bottomed out at 47.2 in February 2024. Although sentiment has generally improved since then, it only entered growth territory once, in May. Automotive production volume fell by more than 10% year-on-year in H1 2024, though there are early signs of an upswing in semiconductor manufacturing equipment.

In contrast, South Korea (light-green line in Fig. 1 and Fig. 3), which traditionally accounted for just under half of Japan’s sales volume in Machine Vision components sales, presents a more optimistic picture. Industrial production surged by 12.9% year-on-year at the start of 2024, led by automotive manufacturing, and maintained its growth trajectory throughout the first half of the year. Since May, South Korea has led the M-PMI ratings of Machine Vision’s primary target markets, with readings well above 51. With inflation nearing the 2% mark and an uptick in domestic consumption, the Korean economy appears to be leading over all G7 countries in recovering from the post-COVID turmoil.

India and Southeast Asia

India’s (green line in Fig. 2 and Fig. 4) industrial production growth averaged a robust 5% in H1 2024, supported by consistently positive sentiment among purchasing managers, with M-PMI readings ranging between 55 and 59 over the past 25 months. However, Prime Minister Modi’s ability to implement pro-economic policies has been complicated by a diminished majority following June’s general election. The much-anticipated reform of the Indian legal system now seems less likely, potentially hindering accelerated growth. Nevertheless, the relocation of production capacity from China remains a key driver of the boom in India’s manufacturing sector.

Automotive manufacturing is a cornerstone of Indonesia’s economy and labor market. Yet, in the first seven months of 2024, automotive production volume plummeted by 18.5% to 666,000 units. Initiatives like Subang Smartpolitan aim to boost manufacturing automation in Indonesia and beyond, particularly in automotive production, laying the groundwork for increased use of Machine Vision technologies. Simultaneously, Foreign Direct Investments, largely directed towards local manufacturing facilities, increased by 16% year-on-year in H1 2024. We expect the manufacturing sector in this country of 270 million people to expand in the coming years.

Thailand’s politics

are in turmoil, the Philippines are struggling to develop a maritime oil field

crucial for their energy supply amid disputes with China, and the potential

annexation of Taiwan by China remains a matter of military success and economic

risk. With a poor 2023, Taiwan recorded an average year-on-year industrial

production growth of 10.5% in H1 2024, primarily driven by its chipmaking

activities. Southeast Asian countries with political stability, such as

Vietnam, Malaysia, and Singapore, also show positive sentiment scores and solid

growth rates in their manufacturing output, offering great opportunities for

cost-effective, easy-to-use Machine Vision technologies.

Short- and long-term strategies for Machine Vision players

In the absence of growing end-user consumption, the lack of skilled workers, increased labor costs, and expanding quality and profitability requirements continue to drive manufacturing automation and, consequently, machine vision sales. The purchasing power of average citizens in many developed countries is gradually eroded by inflation, political policies, and public debt, leading to long-term dampened consumption.

Today’s developing countries, which will be home to over 6 billion people by 2050, are and will continue to be the primary drivers of global growth in end-user consumption. These consumers are beginning to improve their living standards with low-cost products that need to be produced as cost-effectively as possible. Over the coming decades, the demand for products of higher quality, complexity, and value will grow.

Ambitious Machine Vision component and solution OEMs can benefit from these market developments with cost-optimized designs and a focus on applications with clear business cases in these countries.

Would you like to learn more about market trends by country or the developments in specific industries?

The team for Machine Vision market research Vision at Vision Markets is happy to support you with custom analyses. We answer crucial questions and help you design winning business strategies based on your technology stack, market access, and growth targets. Reach out to us now!

Don’t miss our future market updates and be the first to receive them! Subscribe to our VisionCrunch business newsletter today!

The global agriculture and food industry employs over 1 billion workers and faces the challenge of feeding 10 billion people by 2050. Price pressure, regulatory requirements, and labor shortage make the food industry one of the most important application areas for Machine Vision technologies. According to Vision Markets’ latest report of the Machine Vision components market, the food industry surpassed the revenue mark of 1 billion USD with Machine Vision components in 2022 for the first time.

Disclaimer: The information provided in this article is for informational purposes only and should not be considered investment advice. The author is not a registered investment advisor and is not affiliated with any brokerage or investment firm. Investing in the stock market involves risk, including the loss of principal. Readers should conduct their own research and consult with a financial advisor before making any investment decisions.

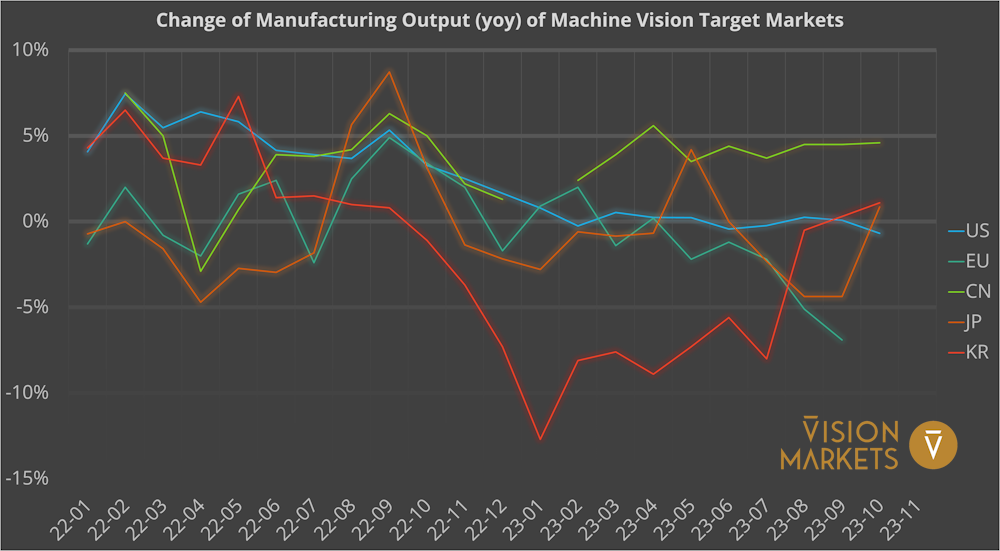

Calling 2023 a bumpy road appears to be a rather euphemistic label from the perspective of quite some Machine Vision players. The Manufacturing Output of the G7 countries entered a major recession (see Fig. 1) and the recently published October data did not spark any optimism for changing this trend.

Fig. 1: Year-over-year Change of the Manufacturing Output in the key target markets of Machine Vision, latest readings

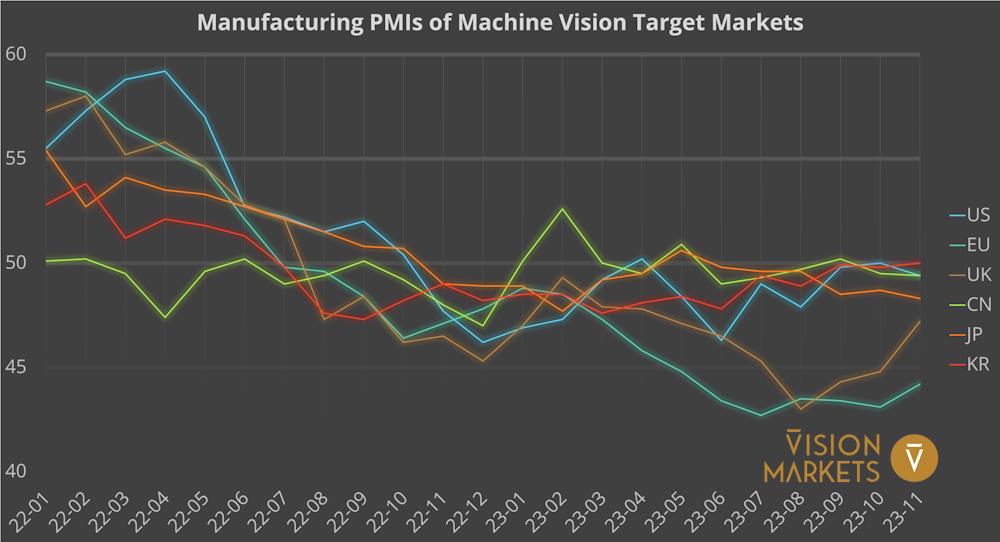

The forward-looking economic indicators of Manufacturing PMIs by country remained in the contraction area below the 50-points line for the majority of 2023 (see Fig. 2). Europe’s PMIs point towards a remarkable recession in the secondary sector with Germany (see Fig. 3) leading the downward trend.

Fig. 2: Manufacturing PMI readings in the key target markets of Machine Vision, Jan. 2022 to Nov. 2023

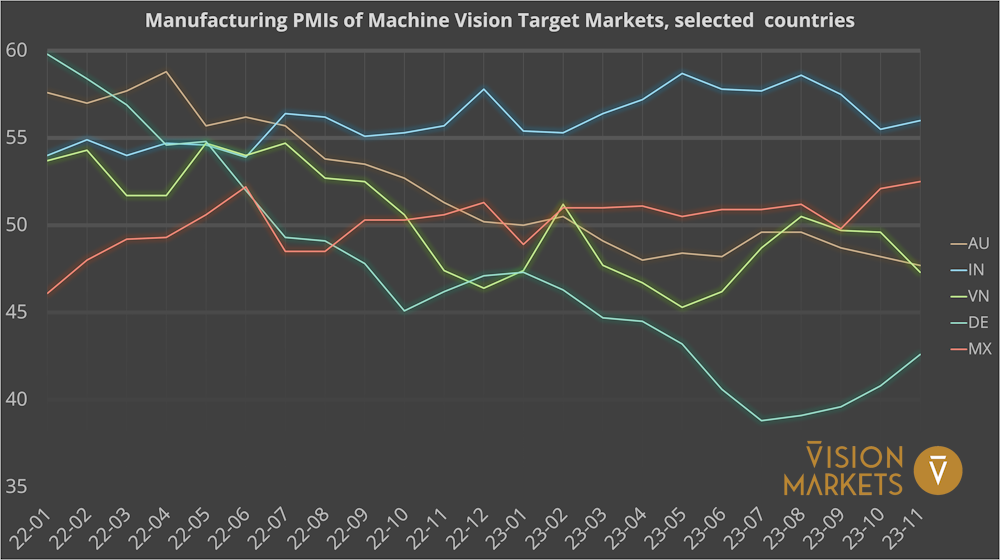

China, the Factory of the World, is the largest single market for Machine Vision since 2022. However, the source-domestic policy of the ruling party favors domestic suppliers at the expense of foreign players. Economic and political tensions have prompted western companies to relocate factory sites to “ROW” countries. Fig. 3 shows the positive mood of purchasing managers in India throughout 2022 and 2023. In October and November, also the M-PMI for Mexico brightened the outlook into 2024, while the mood in Vietnam was dragged down by the economic turbulences of its neighbor and biggest trade partner in the north.

Fig. 3: Manufacturing PMIs in selected target countries for Machine Vision, Jan. 2022 to Nov. 2023

What are the Upcoming Business Opportunities in the Agriculture and Food Industry?

Food producers can be seen as end-users of automation technologies such as machine vision. In this highly consolidated market, ten giant enterprises dominate the global landscape with an annual revenue of 0.5 trillion $ and a forecasted nominal (i.e., not inflation adjusted) growth of 10% in 2023. Nestle alone will contribute 100 bn$.

However, their

profitability suffered recently, especially from increased energy and labor

costs. Furthermore, supply issues from declining crop yields attributed to

climate change and Russia’s invasion in Europe’s breadbasket Ukraine have led

to higher expenses. Still, companies like Coca Cola stand out with an

operational profitability north of 30%. The financially strong companies with

billions of dollars of quarterly earnings have realized already in the

2000-years that Automation and Machine Vision provide them with competitive

advantages. Most of them have built in-house resources and top-notch Machine

Vision expertise for enhanced food processing, quality control, and packaging.

Hence, these companies specify or even develop their own vision systems today.

The sector of machinery

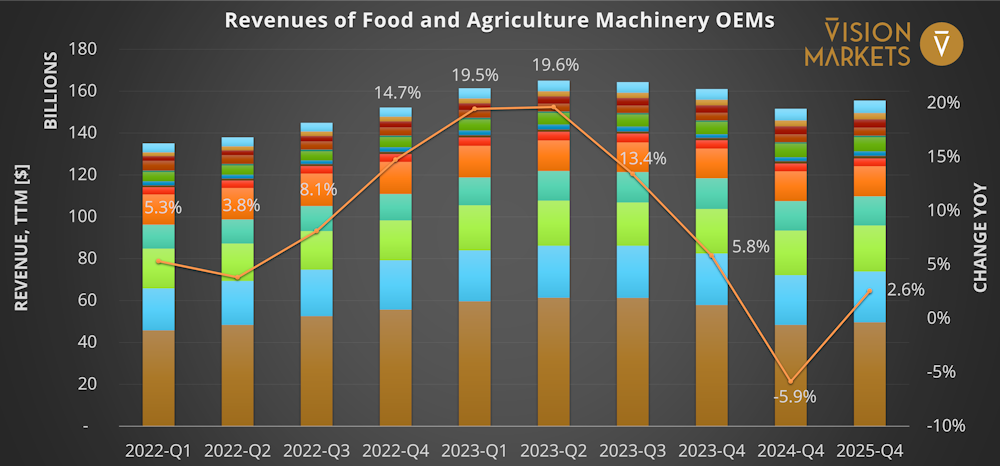

for agriculture and food production, however, is far more fragmented. Fig. 4

shows the aggregated 12-month revenues of the top-13 OEMs of agricultural

machinery as well as machinery for food and beverages summing up to 164 bn$ in the

period ending Q2 2023. The Q4 values for 2023 to 2025 are analysts’ estimates.

Fig. 4: Aggregated trailing twelve months (TTM) revenue of OEMs of machinery for agriculture and food, including year-over-year (YoY) change rate.

While the manufacturing industry in G7 countries and beyond faced a downswing in 2023, the agriculture machinery and food machinery industry will show a combined annual growth of 5.8%. The forecast for 2024 is rather heterogenous for the two segments. The tight monetary policies of central banks with higher-for-longer interest rates are curbing the appetite to invest into high-value agriculture equipment. This leads to an estimated YoY decline in revenues by 9% in 2024 while the revenues of food machinery OEMs should grow by 3 to 5%. Hereby, the German Krones AG leads the estimations among the monitored enterprises with a 9+% growth.

Growth Driven by the Market, Innovation, and Subsidies

The food industry is the biggest employer, globally, and still doesn’t find enough workers, at least in the western hemisphere. A growing world-population calls for more output and higher productivity. Fierce competition and consumer wallets tightened by inflation require maximum yield and cost savings. Stricter regulations on allergens and pollutants as well as consumer expectations on esthetics and the preservation of healthy nutrients call for strict quality assurance measures.

One of the key solutions to these challenges is Industrial Automation, which uses various methods to enhance the processes of the food industry. Machine Vision is one of the most versatile and powerful methods, as it uses cameras, sensors, and artificial intelligence to perform a variety of tasks, such as:

Vision-guided robots for the reduced application of weed killers, pesticides, and fertilizers and for harvesting.

Autonomously driving tractors based on cameras, lidar, radar, and GPS navigation.

Sorting and grading systems that can inspect bulk products using multi-spectral or hyperspectral imaging, or geometric gauging.

3D vision guided robots that can cut meat and package products with precision and speed.

AI-vision based anomaly detection and quality inspection that can identify defects and contaminants in grain, fruits, vegetables, bakery products, etc.

When they meet the expected price point of the cost-sensitive food industry, these technical innovations will enable impressive growth rates in the coming years. For example, six studies from different research agencies expect the market for Agricultural Robots to grow at a compound annual growth rate (CAGR) of 19 to 35% from 2021 to 2026, reaching a value of 9 to 20 bn$ by 2025.

The market for such advanced agriculture and food processing techniques is not just limited to the western world. Emerging countries with a freaking growth of population also see the need to increase their productivity in this area. India, for example, has launched a Production-Linked Incentive Scheme for the Food Processing Industry (PLISFPI) worth 109 bn INR (~1.3 bn$) of subsidies to generate an additional output of food at a value of 4.0 bn$ to feed the Indian population but also for export.

Innovative Machine Vision technologies are a game-changer for the food industry, as they improve the efficiency, competitiveness, and profitability of the entire food industry.

Vision Markets analyzes the food industry as part of its continuous market research activities including its key players, emerging applications, start-up companies, and investments. Please contact us for further information and opportunities for your business.

Getting prepared for the future

Despite all economic concerns, the need for yield, quality, flexibility, and cost-cutting drives manufacturing automation across the globe. The Industrial Production Outputs and Manufacturing PMIs are important data points but just a small part of over 100 economic indicators, industries, and companies that Vision Markets is constantly including in its continuous analysis of the machine vision market. Especially for business planning for the next fiscal year and further strategy development, the unique market insights by the researchers of Vision Markets provide data-driven decision-making support. Our team of business consultants consists of former CEOs and executives of major machine vision corporations. They facilitate the development and implementation of successful growth strategies for ambitious machine vision players.

Don’t miss our future market updates and be the first to receive them! Subscribe to our VisionCrunch business newsletter today!

After growing by 2.9% year-on-year in 2022 (OECD), the US manufacturing output (blue line) has been hovering around zero growth since early 2023, with a slight downward trend. The September reading was the second positive one in a row, but it did not indicate any change in the trend, at only 0.08% growth. The US Manufacturing PMI also confirmed the stagnation of industrial activity, with 49.8 points in September and a preliminary reading of 50.0 for October. On a positive note, manufacturing capacity utilization rose by 0.2% to 79.7% in September, matching its long-run average from 1979 to 2022.

However, the overall US economy delivered the strongest quarter-on-quarter GDP growth of 4.9% (seasonally and inflation adjusted) in two years in Q3, thanks to consumer spending defying higher prices, rising interest rates, and widespread recession forecasts. The US labor market is extremely strong, leading to an unemployment rate below 4% for 20 consecutive months. Consumers’ mortgages as well as a good share of corporate mortgages have fixed and favorable interest rates. Thus, the impact of the FED‘s rate hikes will only fully materialize when those mortgages are due and need to be refinanced with new contracts.

For 2024, The Economist‘s market intelligence unit predicts a GDP growth of less than 1% for North America, which would be the lowest growth among all economic regions. Wall Street’s common sense, however, points more towards a mild recession in 2024, driven by tighter monetary policies fighting the inflation and wage spiral as well as the trade tensions with China and the detrimental impacts of global warming. The US GDP depends on consumer spending by 70%. Hence, a recession in the national GDP does not necessarily imply a recession in industrial output, considering the re- and near-shoring initiatives of supply chains supported by Bidenomics with its US CHIPS Act (analysis by PwC) and Inflation Reduction Act (analysis by McKinsey).

The recession of the manufacturing industry in the EU (cyan line), especially in Germany, is worsening. The EU manufacturing output plunged to -5.1% in August, the lowest level since the 2008-2009 financial crisis. The M-PMI, which measures the activity of purchasing managers in the manufacturing sector, stabilized slightly above its July low at 42.7 but remained at a devastating 43.4 for September. These five months with readings below 45 indicate a long-term and severe downward trend.

Germany, which is expected to become the world’s third-largest economy in 2023 overtaking Japan, is suffering from multiple factors that are hurting its manufacturing sector. Some of these factors are: China’s efforts to reduce its dependence on foreign technologies and increase its domestic production; the trade tensions and tariffs imposed by the US; the environmental regulations and policies that require a transition to cleaner and more efficient technologies; and the lack of skilled workers and digitalization in most industries. Eventually, the German association VDMA reported a YoY decline of -16% in machinery orders from June to August 2023, wherein orders from the Eurozone fell behind by -14%.

Besides Manufacturing, which is our focus in this economic trend series, the Logistics sector in Europe is suffering. In Germany alone, e-commerce revenues dropped by 14% in Q3 2023 YoY.

Unlike the other economies here, China’s manufacturing output has remained well in positive territory throughout 2023. According to official figures, the manufacturing output grew by 4.5% in both August and September 2023. On average, growth will be between 4 and 5%, despite China’s huge manufacturing GDP in the denominator. The “Made-in-China” policy makes it increasingly difficult for non-domestic vendors to benefit from this growth, as domestic suppliers are favored. Moreover, as economic and political relations are worsening and the fear of an invasion of Taiwan rises, western giants in semiconductors and electronics are relocating production sites to India, Thailand, Vietnam, Singapore, and other “ROW” countries – see below.

Japan & Korea: Waiting for the Semiconductors Industry

The manufacturing output of South Korea (red line) is still in negative growth territory, but it showed a significant and surprising jump to -0.5% in August, from -8% in July. Korea’s defense industry benefits from large orders from NATO countries in their support of Ukraine against Russia. However, Asia’s fourth-largest economy is struggling with weak demand in its core export markets, especially in Europe

Vision Markets’ quarterly monitor of the top OEMs in Semiconductor Manufacturing Equipment reported their revenue to be 15.3 billion USD in Q2 2023, which constitutes a decline of -8.5% year-on-year and -4.8% quarter-on-quarter. Korea, with its exposure to the semiconductor industry, is suffering from its current weakness. Yet, the SEMI association reports that the semiconductor industry bottomed out at the end of the first half of 2023, and has since started a recovery, setting the stage for continued growth in 2024. All segments are projected to log year-on-year increases in 2024, with electronics sales surpassing their 2022 peak.

Japan (orange line) is seeing its Manufacturing PMI decline to 48.5 in September. Japan’s key manufacturing industries are expected to grow by 1.8% in 2023, mainly supported by Automotive and Medical products growing between 2.2 and 2.5%. The total for 2024 is said to be in a similar range, but the long-term outlook shows a continued deceleration of growth in industrial manufacturing. The Japanese yen has lost about 13% in valuation against the US dollar since the beginning of 2023, as a result of Japan’s struggling economy and different monetary policies. The reduced costs of products from Japan can hardly compensate for the fact that China’s OEMs and users have turned into competitors rather than customers for Japanese companies.

Rest of World (RoW): Opportunities in Southeast Asia

Purchasing managers of manufacturers in the emerging markets have lost a bit of confidence since our last report in August. But let’s take a look one by one.

Mexico is coming from a growth in Manufacturing GDP of 5.2% in 2022 vs. 2021. Since September 2022, Mexico’s M-PMI readings were all slightly above 50, except for January this year. This resulted in a growth of 2.7% in industrial production output, approximated by the average monthly YoY trend in H1 2023. The average M-PMI reading of 50.6 in 2023 was undercut by a drop to 49.8 in September dropping into the contraction area correspondingly. Despite all the billions of USD investments by automakers and heavy industry into new factories, Mexico is dependent on the demand for goods of its big neighbor in the north. As described above, the US manufacturing industry is shaky with detrimental effects on Mexico’s OEMs.

Vietnam contributed an added-value manufacturing output of 90 bn$ in 2021 and as such it is a tiny player in global terms. Being the closest emerging market to China, Vietnam attracted billions of manufacturing investments beyond its traditionally strong textile industry. Vietnam’s M-PMI showed high volatility in H1 2023 coming from positive territory in 2022 declining to its lowest reading of 45.3 in May. It recovered to a flat to growth-suggesting reading of 50.5 in August but dropped slightly back below the neutral 50 points line in September. China is the second largest export destination of Vietnam, thus, the weakness of its northern neighbor harms manufacturing activities. Furthermore, Vietnam is known for its manufacturing capacities of rather low-cost consumer goods. Globally, and especially in Europe, consumer spending is contracting. As Vietnam’s power and transportation infrastructure keeps improving, Machine Vision players are witnessing growing demand to automate all the new factories being built.

India‘s purchasing managers of manufacturers are among the most enthusiastic when it comes to near-term growth. Despite the drop to 57.5 in September from close to a record-high 58.6 in August, the Indian manufacturing industry is growing the fastest among all economies in Southeast Asia in absolute terms. With a population of over 1.4 billion and a growing per capita GDP of 2,257 USD in 2021, India features a large domestic market, low labor costs, and a well-educated workforce. Players like Cognex, Edmund Optics, and OPT Machine Vision, have set up their own marketing, sales, and support centers in India. German sensor OEMs Wenzel Group and Schäfter+Kirchhoff has just recently opened R&D centers and manufacturing facility in India showing the growing importance of this region for Machine Vision players.

Getting prepared for the future

Despite all economic concerns, the need for yield, quality, flexibility, and cost-cutting drives manufacturing automation across the globe. Industrial Production Output and Manufacturing PMI are important but they are only a small part of over 100 economic indicators and companies that Vision Markets is constantly including in its continuous analysis of the machine vision market. Especially for business planning for the next fiscal year and further strategy development, the unique market insights by the researchers of Vision Markets provide data-driven decision-making support. Our team of business consultants consists of former CEOs and executives of major machine vision corporations. They facilitate the development and implementation of successful growth strategies for ambitious machine vision players.

Don’t miss our future market updates and be the first to receive them! Subscribe to our VisionCrunch business newsletter today!